What If a Simple Home Loan Balance Transfer Could Significantly Reduce Your Long-Term Financial Burden?

Discover how moving your home loan to a new lender can save you lakhs in interest, lower your EMIs, and help you achieve debt freedom faster.

What If a Simple Home Loan Balance Transfer Could Significantly Reduce Your Long-Term Financial Burden?

Owning a home is a dream for many, but the reality of a 20-year mortgage can often feel like a heavy weight on your shoulders. Over the course of two decades, the interest you pay can sometimes equal—or even exceed—the actual amount you borrowed.

But what if you didn’t have to stick with the original terms of your loan? What if a simple strategic move could save you lakhs of rupees and shave years off your debt? This is where the power of a Home Loan Balance Transfer (HLBT) comes into play.

The Silent Cost of "Set It and Forget It"

Most homeowners treat their home loan as a "set it and forget it" commitment. However, the financial market is dynamic. Interest rates fluctuate, and your own creditworthiness improves over time. If you took your loan a few years ago, you might be paying a much higher rate than what is currently available to new customers.

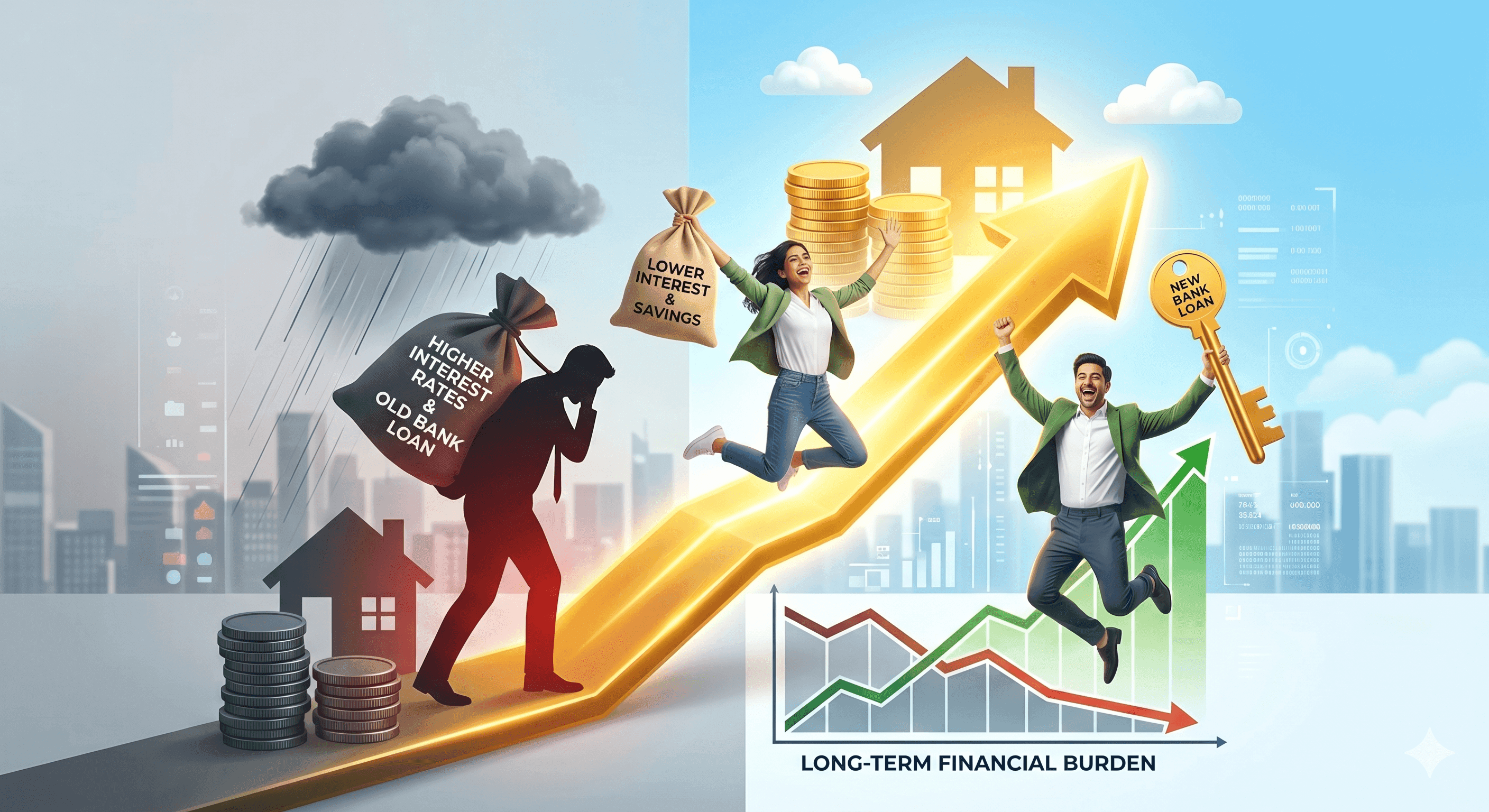

How a Home Loan Balance Transfer Works

A balance transfer is the process of moving your outstanding loan principal from your current lender to a new one. The new bank pays off your old loan in full, and you start paying your monthly EMIs to the new bank—typically at a much lower interest rate.

The Triple Benefit of Switching

1. Massive Interest Savings

The most immediate benefit is the reduction in interest. Even a seemingly small drop of 0.50% to 1% in your interest rate can result in savings of several lakhs over a 15-year remaining tenure.

2. Lower Monthly EMIs

If your primary goal is to increase your monthly disposable income, a balance transfer allows you to reduce your EMI. This provides immediate relief to your monthly household budget.

3. Accelerated Debt Freedom

Alternatively, you can choose to keep your EMI amount the same even after the rate drops. This ensures that a larger portion of your payment goes toward the principal amount, effectively reducing your loan tenure. You could finish your loan years earlier without paying a single extra rupee out of pocket.

When Should You Make the Move?

A balance transfer is a powerful tool, but it should be used strategically. It is most effective when:

- You are in the early stages of your loan: Since interest is front-loaded, switching in the first 5-7 years yields the highest savings.

- The rate gap is significant: Look for a difference of at least 0.50%.

- Your credit score has improved: A higher score gives you the leverage to negotiate the lowest possible rates.

The "Hidden" Advantage: The Top-Up Loan

When you transfer your loan, many banks offer a "Top-Up" facility. This allows you to borrow additional funds at home loan rates (which are significantly lower than personal loan rates) for renovations, business expansion, or even education.

Conclusion

Your home loan doesn't have to be a static burden. By staying proactive and exploring a balance transfer, you can take control of your financial future. It’s not just about moving a loan; it’s about optimizing your wealth.

Need Expert Guidance?

Navigating the paperwork and finding the best lender can be overwhelming. I am here to help you calculate your potential savings and manage the transition seamlessly.